Note to the reader: This is the twelfth in a series of articles I’m publishing here taken from my book, “Investing with the Trend.” Hopefully, you will find this content useful. Market myths are generally perpetuated by repetition, misleading symbolic connections, and the complete ignorance of facts. The world of finance is full of such tendencies, and here, you’ll see some examples. Please keep in mind that not all of these examples are totally misleading — they are sometimes valid — but have too many holes in them to be worthwhile as investment concepts. And not all are directly related to investing and finance. Enjoy! – Greg

Technical analysis offers an unbiased truth about the markets. If one is going to follow and utilize a particular discipline, hopefully they have done a thorough investigation as to the benefits and pitfalls of that discipline.

Today I’ll share a short story from the mid-1970s, a period of my life when I was a Navy fighter pilot, and, of course, knew everything. I had a few thousand dollars that I wanted to invest. I honestly can’t recall my source for research, but I’m almost positive I didn’t pay for any of it; probably a trip to the Public Library and probably the Value Line Investment Survey. This is a giant black ring binder with a single page dedicated to a single stock in the Value Line universe of about 1,700 issues. I know the research was quite thorough, and it probably took me a few months to even work up the nerve to actually speculate (I called it invest back then) in the market. I don’t even recall the small brokerage firm I used, but I do remember that discount firms were being talked about, though none were in existence then (I think). There was no FNN (Financial News Network), CNBC, Fox Business, or Bloomberg television in those days.

My research efforts involved the typical fundamental review looking for stocks that met a host of different criteria, using ratios such as price to earnings, price to dividend, price to book, and so on. I do know that the price to sales ratio had not been created yet; I think it was developed by Ken Fisher in the 1970s and became widely used in the 1980s. So I bought two stocks in late 1972; I remember that one of them was UAL (United Airlines). Clearly my bias for aviation was part of the decision—a bias that this book is trying to teach is totally wrong.

For two months, they went straight up. I have to be honest, I thought I was truly brilliant. I was euphoric. Then, in early 1973, my brilliance turned to anxiety when the prices of both stocks started to decline. Fear of losing money was now dominating my thought process. Strangely, nothing entered my mind in regard to selling those stocks, or putting a stop loss order in (I doubt I even knew what that was then), I just knew I was right and was going to prove it. Well, as I recall, I held those two stocks until sometime in 1975. They had declined with the market and, by the end of 1974, were down 75 percent from where I bought them. I had no stops, I had no plan, I had no money management, I had nothing but an ego that kept me totally wrong for two years. The market started up in early 1975 and I was so happy to unload them for a few percentage points above their bottom, I swore I’d never gamble in the market again. However, I remember that it sure made me feel good to buy a stock, because the financial ratios were good. Fortunately, I quickly learned that feeling good has very little to do with making money in the markets.

It was then that I read a book, suggested by a good friend, called The Art of Low Risk Investing, by Michael Zahorchak. I had previously read a few other books on technical analysis, but none of them involved a process; they usually dealt with chart patterns, and so on. Zahorchak offered a complete and rational technical process to investing. The book has long been out of print, but I’m sure you can find it on eBay or somewhere. If you are having doubts about technical analysis, this book will correct that. I have never deviated from technical analysis since that experience in the mid-1970s; I believe it is the best way to help investors control their emotions during the investment process.

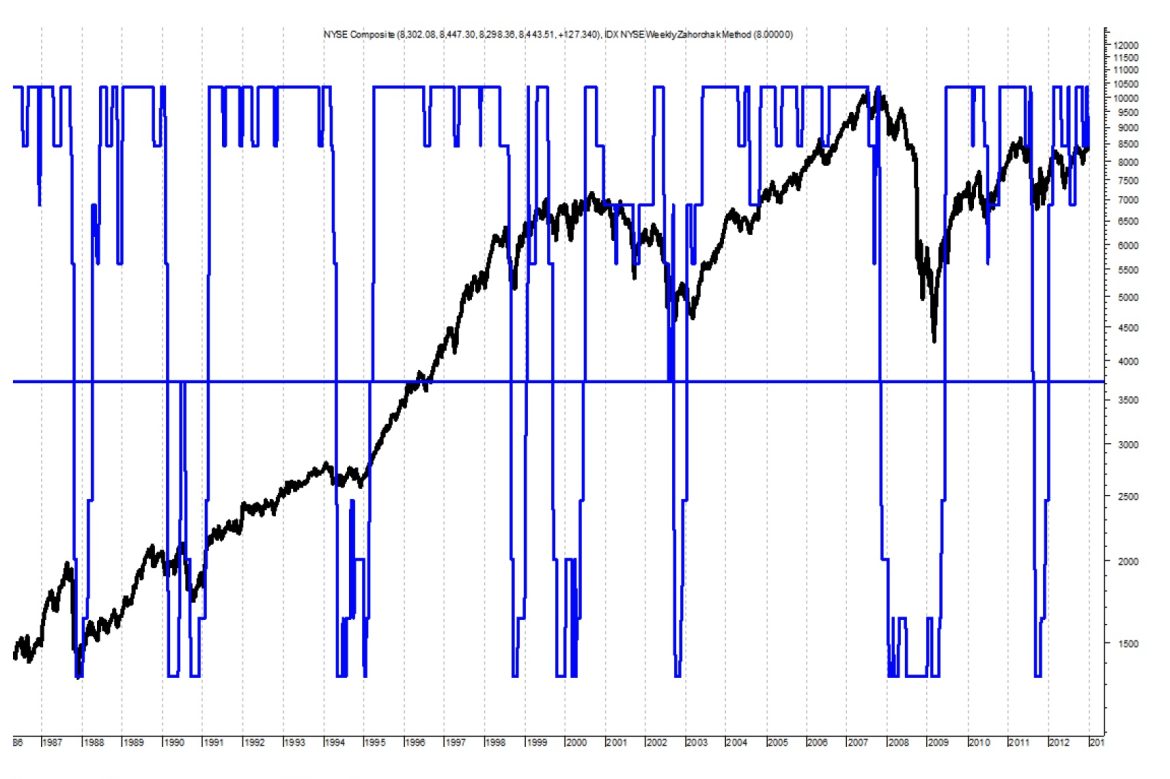

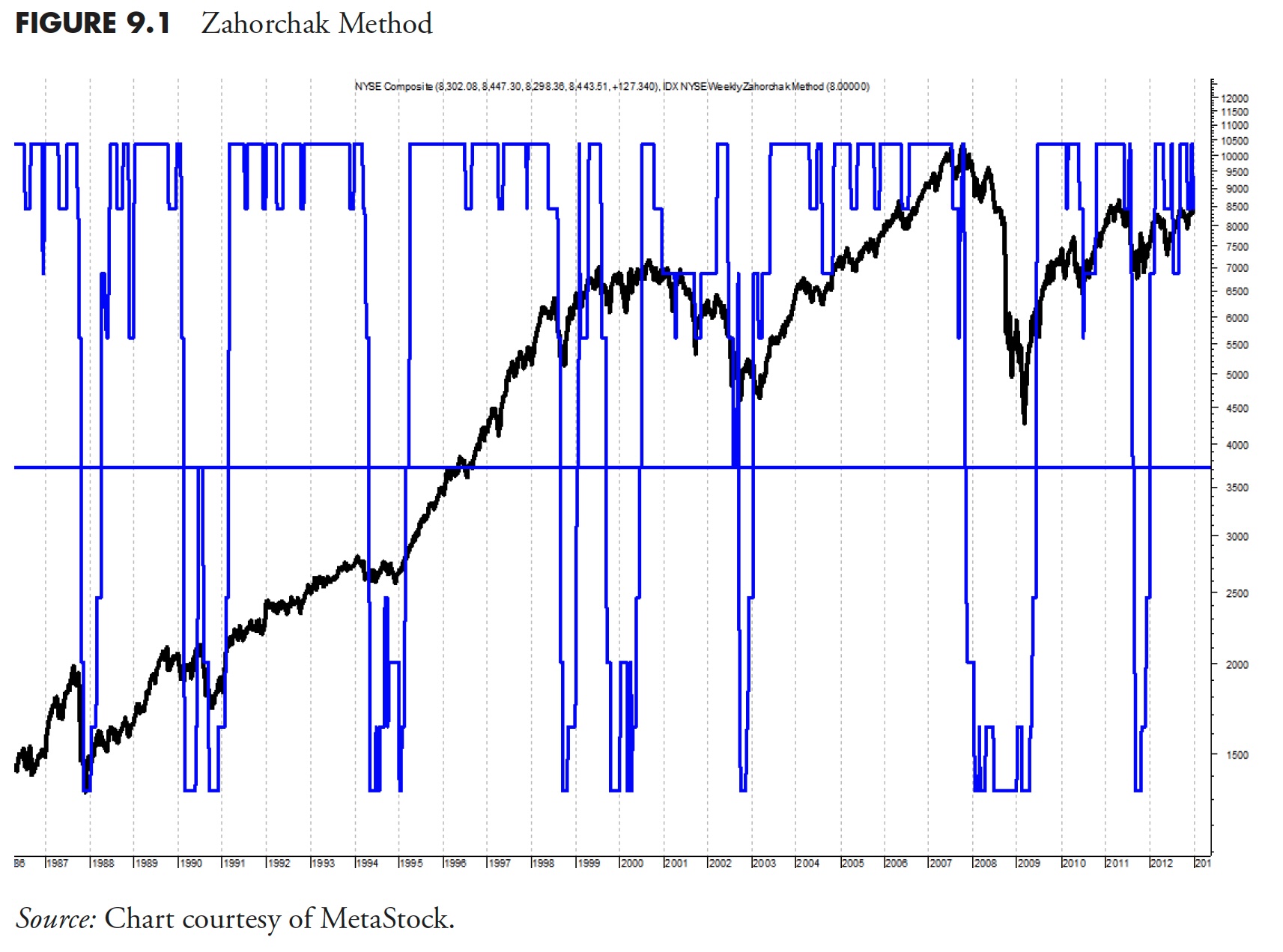

Figure 9.1 shows the NYSE Composite Index with my interpretation of the Zahorchak method overlaid. Whenever the Zahorchak method line is above zero (horizontal line), one should be invested in equities; when below zero, one should be invested in cash or cash equivalents. One could further fine-tune it by using various levels for different asset commitments to enhance the process. The Zahorchak method uses only weekly data, with moving averages of 5, 15, and 40 on the NYSE Composite Index and the NYSE Advance Decline Line for its signals. The same process is then applied to stocks for selection. A complete set of rules is given on how to make trades from that data.

Now, within technical analysis, there are many varied approaches. Many of which I have tried, but was not successful. I like to say that I have a master’s degree in what not to do, as those lessons came at a significant cost. As I have aged, I have slowly learned not to speak in absolutes about the market, as any approach that one can use to be successful is the right approach for that person. Just because I don’t care for some approach does not mean that someone else cannot use it successfully.

There are different types of market analysis. The most widely used is fundamental analysis, which focuses on multiples or fundamental ratios. Almost 90 percent of these ratios use price, usually in the numerator or sometimes in the denominator. Price earnings ratio, price to sales, price to dividends, price to book ratio, and so on, are just a few of them.

Technical analysis, however, is the analysis of price. Price is what we buy. When you buy a stock, you are not buying the earnings, the products, the management, dividends; you are buying the stock at a market-generated price. Those other things might be why you buy it, but they are not what you are buying, you are buying the stock, not the company.

Trend determination is the trend of the price that we are analyzing. Trend analysis is a significant part of what this book is all about. Breadth analysis is a derivative of price movement; it is a critical contribution to technical analysis. Relative strength analysis is the analysis of one group relative to another; one example is the relationship between small-capitalization stocks and large-capitalization stocks. However, most importantly, technical analysis bridges the gap between doing the analysis and taking action—it is just the next step.

What is Technical Analysis?

Martin Pring says the art of technical analysis is to identify trend changes at an early stage and to maintain an investment position until the weight of the evidence indicates that the trend has reversed. Although there are other definitions, Pring’s definition is the one I agree with. It is primarily used two ways: predictive and reactive. Most newsletter writers, television experts, and brokerage firm analysts use it to predict the market. The reactive mode means that it is used to measure what the market is doing, then just react to that information. The subject of this book is all about the latter. React, don’t predict.

For additional reading on technical analysis, I strongly recommend Technical Analysis, by Charlie Kirkpatrick and Julie Dahlquist. It is the best single volume on technical analysis there is.

I Use Technical Analysis Because…

It is something we can believe in and rely on. It removes the destructive emotions of fear, hope, and greed.

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.” — Benjamin Graham (the great value investor)

It keeps our perceptions clear.

“It ain’t what you know that gets you into trouble, it’s what you know for sure that just ain’t so.” — Mark Twain

And the absolute most important thing technical analysis does is it gives us discipline.

I want to share a story with you. I have been on a diet my entire adult life. Seriously! Last spring (as of this writing), my wife and I were driving in the north Georgia mountains one Sunday afternoon. I stopped at an old filling station for gas. It had the old-style pumps, so I had to go inside to pay for the gas. I see a candy bar near the register and buy it. As I ‘m walking back to the car, I can see my wife giving me “that look.” You know that look, don’t you? I get in the car and she says, “You just don’t have any discipline.” I said, “That’s not true, because you don’t know how many of these I wanted.”

I tell that story because discipline is not a knob or a lever that you can subjectively set each day. Discipline is something that must be instilled into your life and your work. I think everyone will agree that when it comes to investing, a disciplined approach is probably going to be a better approach. I’ll take that one step further and say that a disciplined life is probably going to be a good life. Discipline is a critical element for success in the stock market and in life.

The Challenge of Technical Analysis

“I know of no way of judging the future but by the past.” — Patrick Henry

Warning: I share passionate opinions in this section. As of this writing, I am approaching 40 years of being actively involved in technical analysis; you can assume correctly that I have some strong opinions on things. To be perfectly honest, those opinions have changed from time to time, but I do want to share them here. Does this mean that I think I am correct and anything I question is wrong? Not at all, most of technical and, in particular, market analysis is arguable and controversial. I just focus on what works for me.

What is technical analysis? Books are filled with definitions and interpretations on technical analysis. A significant part of technical analysis is the art of studying the past, attempting to identify a pattern or event that seems to represent or reflect the market being studied, and then believing that it will work with some certainty in the foreseeable future.

My definition for technical analysis and my adherence to using it comes from a belief that everyone needs something to believe in or rely on. I believe in technical analysis because of its close relationship to the supply and demand of the market. Fundamental analysis, which is by far a more popular method of analysis, is generally flawed in that it does not address the issue of “when.” When should I buy or when should I sell? Researching the hundreds of different fundamental ratios is the full-time job of thousands of securities analysts. However, think about this simple fact. Almost all fundamental ratios involve price. So why not analyze price? Most forms of technical analysis do just that.

Is technical analysis the same as market timing? Sometimes it is, sometimes it isn’t. Market timing has received a bad rap, especially by those who believe it is a process by some who blindly follow some over-optimized mechanical system without utilizing money management or an asset commitment plan. In that regard, its bad rap is appropriate. The analysis of risk and reward is not market timing in the sense that many think of when using that often misused term. Determining when the market has too much risk is not market timing, but prudent and discretionary investment decision-making. Next time you hear a brokerage firm analyst mention that no one can time the market, or that technical analysis does not work, ask to see his record during the bear markets of 2000 to 2002 or 2007 to 2009. Heck, he probably wasn’t a stockbroker then anyway. I hate it when I call salespeople stockbrokers. They are not stockbrokers, as that is what the company they work for is called; they are salespeople for a stockbroker. I feel better now.

I have a cassette tape that I received from Sedge Coppock, the founder of the San Antonio firm, Trendex. This was in 1983 when I was heading a group of technical analysts in Dallas and wanted him to come up and speak to us. He declined, but sent a tape, which was about 30 minutes in length, in which he said how inept most investors were at controlling their emotions and that even worse than that was when they sought advice from a stockbroker. Sedge did not hold stockbrokers in high regard. I was fortunate to attend the Market Technician’s Association annual seminar in Naples, Florida in 1989 when Edwin Sedgwick Chittenden Coppock received their highest award, the MTA Annual Award. He passed away the next year.

Another challenge to technical analysis is that of whether it is an art or a science. I cannot believe anyone would seriously ask this, and suspect the question comes almost totally from the nonscientific or the innumerate among us. I do believe that scientists, engineers, and mathematically inclined investors migrate toward technical analysis over time because of its ability to look back in history and see how supply and demand played out. It is certainly a more analytical approach to market analysis.

Many claim that technical analysis is science. My response is that the person making the claim is neither a scientist nor an engineer, and clearly doesn’t know the difference between art and science. Finance and economics are considered social sciences, which is a wide swath into the wrong direction. Neither are science, they are arts. You don’t get a bachelor of science degree in them; you get a bachelor of arts degree.

Here’s the difference between art and science. Science is when you can reliably repeat something within predefined parameters. For example, I know that at sea level, with the ambient temperature at 59 degrees Fahrenheit or 15 degrees Centigrade (59 – 32 = 27. 27 / 9 = 3. 3 x 5 = 15), and the atmospheric pressure is 29.92 inches or 1,013 millibars, that pure water H2O, in laboratory conditions, will boil at 212 degrees Fahrenheit or 100 degrees Centigrade. I’ll bet a large sum of money on it. I can’t think of anything in finance, economics, or technical analysis in which I would do that.

Those who get excited and experience a warm feeling about the overused adjectives of quality, strong, healthy, and so on, when Wall Street talks about investing in specific companies, are surely the ones who think technical analysis is witchcraft. Years ago, I used to be entertained by watching Wall Street Week, and was humored by the fundamental analysts who would talk endlessly about how they liked to pick good quality companies and hold onto them. They then quickly point out the Ibbotson study that shows that equities have performed at about a 9-plus percent annual rate for the past 100 years. Hogwash! While the study is true, it is totally irrelevant as one does not have a 100-year investment horizon, and is therefore not applicable to humans. Most investors have a good 20-year period in which to make their serious investments. There were many 20-year periods in the past 100 years that resulted in negative or inadequate returns. The most egregious example is if you had bought in 1929, you did not break even until 1954; 25 years later. And guess what, getting even is not what investing is all about.

A good detective will tell you that some of the least reliable information comes from eyewitnesses. When people observe an event, it seems their background, education, and other influences unrelated to the observed event, color their perception of what occurred. Most will also be influenced by what they hear from others. This is also amplified by a number of individual studies done by behavior psychologists. In a nutshell, they all agree that groups of people will tend to amplify the consensus view rather than challenge it. A group’s ability to focus on common knowledge and uncover anything new is commonplace. Plus the fact that if someone in the group is acknowledged as an expert, their opinion can totally dominate the thinking for the group and can lead to what is known as the herd mentality. Talk radio is a perfect example of this.

“The riskiest moment is when you are right. That’s when you’re in the most trouble, because you tend to overstay the good decisions.” — Peter Bernstein

I don’t want to turn this into a science book, but I am adamant about correcting the proliferation of bad or incorrect information that exists in the financial markets and by showing you similar misconceptions that you may have believed before is the best way to get your attention. In a previous chapter, there was a discussion about believable misinformation; if you found that you believed one or more of those misconceptions, then how many market-related ones do you also believe?

Technical analysis will let you deal with reality and keep you from falling victim every time the financial news offers their expert opinion on why the markets did today what they did. I remember when the Indonesian earthquake tidal waves killed thousands of people, but you could not begin to know how many during the initial broadcasts. Most news sources were stating guesses anywhere from 15,000 to well over 150,000. Many news sources cannot even keep the number consistent within their own articles. Do you think they can also tell you why the markets did what they did on a daily basis? Stick to technical analysis; it will increase your understanding of the markets, if only by the fact that you are uncovering information about market behavior.

Here are some comments on technical analysis that I read more than 35 years ago in The Commodities Futures Game by Richard Teweles, and believe to be just as valid today. Almost all methods of technical analysis generate useful information, which, if used for nothing more than uncovering and organizing facts about market behavior will increase the investor’s understanding of the markets. The investor is made painfully aware that technical competence does not ensure competent investing. Speculators who lose money do so not always because of bad analysis, but because of the inability to transform their analysis into sound practice. Bridging the gap between analysis and action requires overcoming the threat of greed, hope, and fear.

Technical analysis is the art of analysis that will keep your emotions from being a part of your investment decision making. While not infallible, it certainly gives you the tools to assist in overcoming the human traits of ignorance and bliss. Ignorance is an intellectual state and appears to be chronic in many people as regards to the stock market. Bliss is an emotional state and it characterizes many investors as long as the market is going up. Deluded by emotions, one cannot begin to be successful in the investing arena without some means of controlling greed, fear, and hope. This is what I think technical analysis does best.

Thanks for reading this far. I intend to publish one article in this series every week. Can’t wait? The book is for sale here